TP Corrected: Recurrent Neural Networks for Time Series Prediction

Author

Remi Genet

Published

2025-04-03

!pip install numpy keras jax matplotlib scikit-learn yfinance

Requirement already satisfied: numpy in /usr/local/lib/python3.10/dist-packages (2.2.2)

Requirement already satisfied: keras in /usr/local/lib/python3.10/dist-packages (3.8.0)

Requirement already satisfied: jax in /usr/local/lib/python3.10/dist-packages (0.5.0)

Requirement already satisfied: matplotlib in /usr/local/lib/python3.10/dist-packages (3.10.0)

Requirement already satisfied: scikit-learn in /usr/local/lib/python3.10/dist-packages (1.6.1)

Requirement already satisfied: yfinance in /usr/local/lib/python3.10/dist-packages (0.2.52)

Requirement already satisfied: namex in /usr/local/lib/python3.10/dist-packages (from keras) (0.0.8)

Requirement already satisfied: packaging in /usr/local/lib/python3.10/dist-packages (from keras) (24.2)

Requirement already satisfied: h5py in /usr/local/lib/python3.10/dist-packages (from keras) (3.12.1)

Requirement already satisfied: ml-dtypes in /usr/local/lib/python3.10/dist-packages (from keras) (0.5.1)

Requirement already satisfied: optree in /usr/local/lib/python3.10/dist-packages (from keras) (0.14.0)

Requirement already satisfied: absl-py in /usr/local/lib/python3.10/dist-packages (from keras) (2.1.0)

Requirement already satisfied: rich in /usr/local/lib/python3.10/dist-packages (from keras) (13.9.4)

Requirement already satisfied: scipy>=1.11.1 in /usr/local/lib/python3.10/dist-packages (from jax) (1.15.1)

Requirement already satisfied: jaxlib<=0.5.0,>=0.5.0 in /usr/local/lib/python3.10/dist-packages (from jax) (0.5.0)

Requirement already satisfied: opt_einsum in /usr/local/lib/python3.10/dist-packages (from jax) (3.4.0)

Requirement already satisfied: contourpy>=1.0.1 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (1.3.1)

Requirement already satisfied: python-dateutil>=2.7 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (2.9.0.post0)

Requirement already satisfied: pyparsing>=2.3.1 in /usr/lib/python3/dist-packages (from matplotlib) (2.4.7)

Requirement already satisfied: cycler>=0.10 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (0.12.1)

Requirement already satisfied: fonttools>=4.22.0 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (4.55.8)

Requirement already satisfied: pillow>=8 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (11.1.0)

Requirement already satisfied: kiwisolver>=1.3.1 in /usr/local/lib/python3.10/dist-packages (from matplotlib) (1.4.8)

Requirement already satisfied: joblib>=1.2.0 in /usr/local/lib/python3.10/dist-packages (from scikit-learn) (1.4.2)

Requirement already satisfied: threadpoolctl>=3.1.0 in /usr/local/lib/python3.10/dist-packages (from scikit-learn) (3.5.0)

Requirement already satisfied: requests>=2.31 in /usr/local/lib/python3.10/dist-packages (from yfinance) (2.32.3)

Requirement already satisfied: beautifulsoup4>=4.11.1 in /usr/local/lib/python3.10/dist-packages (from yfinance) (4.12.3)

Requirement already satisfied: frozendict>=2.3.4 in /usr/local/lib/python3.10/dist-packages (from yfinance) (2.4.6)

Requirement already satisfied: pytz>=2022.5 in /usr/local/lib/python3.10/dist-packages (from yfinance) (2024.2)

Requirement already satisfied: html5lib>=1.1 in /usr/local/lib/python3.10/dist-packages (from yfinance) (1.1)

Requirement already satisfied: pandas>=1.3.0 in /usr/local/lib/python3.10/dist-packages (from yfinance) (2.2.3)

Requirement already satisfied: platformdirs>=2.0.0 in /usr/local/lib/python3.10/dist-packages (from yfinance) (4.3.6)

Requirement already satisfied: multitasking>=0.0.7 in /usr/local/lib/python3.10/dist-packages (from yfinance) (0.0.11)

Requirement already satisfied: peewee>=3.16.2 in /usr/local/lib/python3.10/dist-packages (from yfinance) (3.17.8)

Requirement already satisfied: lxml>=4.9.1 in /usr/local/lib/python3.10/dist-packages (from yfinance) (5.3.0)

Requirement already satisfied: soupsieve>1.2 in /usr/local/lib/python3.10/dist-packages (from beautifulsoup4>=4.11.1->yfinance) (2.6)

Requirement already satisfied: webencodings in /usr/local/lib/python3.10/dist-packages (from html5lib>=1.1->yfinance) (0.5.1)

Requirement already satisfied: six>=1.9 in /usr/lib/python3/dist-packages (from html5lib>=1.1->yfinance) (1.16.0)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.10/dist-packages (from pandas>=1.3.0->yfinance) (2025.1)

Requirement already satisfied: idna<4,>=2.5 in /usr/local/lib/python3.10/dist-packages (from requests>=2.31->yfinance) (3.10)

Requirement already satisfied: urllib3<3,>=1.21.1 in /usr/local/lib/python3.10/dist-packages (from requests>=2.31->yfinance) (2.3.0)

Requirement already satisfied: charset-normalizer<4,>=2 in /usr/local/lib/python3.10/dist-packages (from requests>=2.31->yfinance) (3.4.1)

Requirement already satisfied: certifi>=2017.4.17 in /usr/local/lib/python3.10/dist-packages (from requests>=2.31->yfinance) (2024.12.14)

Requirement already satisfied: typing-extensions>=4.5.0 in /usr/local/lib/python3.10/dist-packages (from optree->keras) (4.12.2)

Requirement already satisfied: pygments<3.0.0,>=2.13.0 in /usr/local/lib/python3.10/dist-packages (from rich->keras) (2.19.1)

Requirement already satisfied: markdown-it-py>=2.2.0 in /usr/local/lib/python3.10/dist-packages (from rich->keras) (3.0.0)

Requirement already satisfied: mdurl~=0.1 in /usr/local/lib/python3.10/dist-packages (from markdown-it-py>=2.2.0->rich->keras) (0.1.2)

WARNING: Running pip as the 'root' user can result in broken permissions and conflicting behaviour with the system package manager. It is recommended to use a virtual environment instead: https://pip.pypa.io/warnings/venv

Data Preparation

First, let’s prepare our dataset using yfinance to get historical stock data.

import osos.environ["KERAS_BACKEND"] ="jax"# Environment variable need to be set prior to importing keras, default is tensorflowimport yfinance as yfimport numpy as npimport pandas as pdfrom sklearn.preprocessing import StandardScalerfrom sklearn.model_selection import train_test_splitfrom sklearn.linear_model import LinearRegressionfrom sklearn.metrics import r2_scoreimport kerasfrom keras import layersimport matplotlib.pyplot as plt# Download dataticker ="^GSPC"data = yf.download(ticker, start="2000-01-01", end="2024-01-01")# Compute absolute returns (volatility proxy)returns = np.abs(data['Close'].pct_change())returns = returns.dropna()def create_sequences(data, seq_length, horizon):"""Create sequences for training""" X, y = [], []for i inrange(len(data) - seq_length - horizon +1): X.append(data[i:(i + seq_length)]) y.append(data[(i + seq_length):(i + seq_length + horizon)])return np.array(X), np.squeeze(np.array(y))# Parameterssequence_length =200prediction_horizon =1# Create sequencesX, y = create_sequences(returns.values, sequence_length, prediction_horizon)# Split dataX_train, X_test, y_train, y_test = train_test_split( X, y, test_size=0.2, shuffle=False)early_stopping_callback =lambda : keras.callbacks.EarlyStopping( monitor="val_loss", min_delta=0.00001, patience=10, mode="min", restore_best_weights=True, start_from_epoch=6,)lr_callback =lambda : keras.callbacks.ReduceLROnPlateau( monitor="val_loss", factor=0.25, patience=5, mode="min", min_delta=0.00001, min_lr=0.000025, verbose=0,)callbacks =lambda : [early_stopping_callback(), lr_callback(), keras.callbacks.TerminateOnNaN()]

[*********************100%***********************] 1 of 1 completed

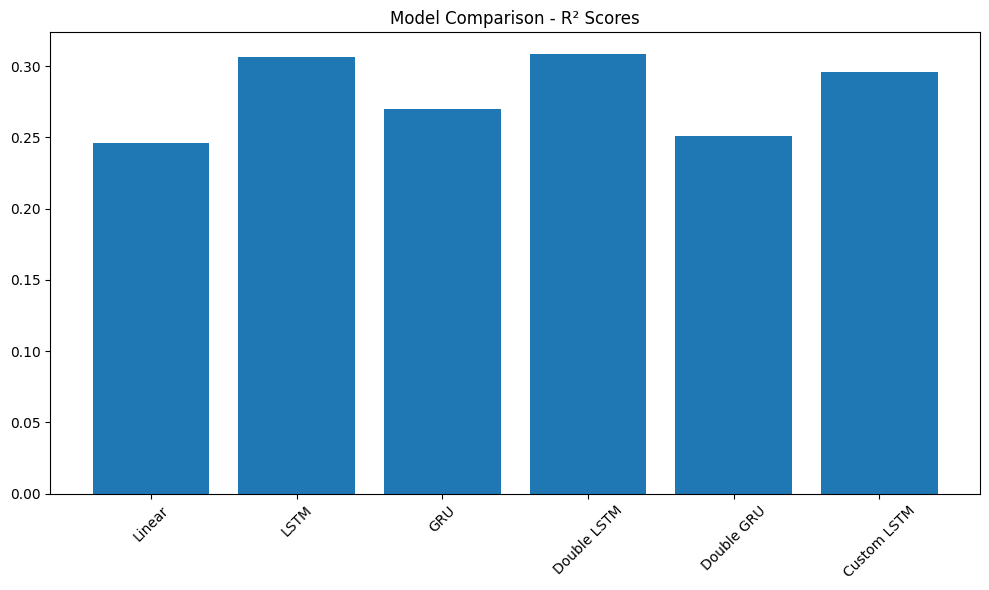

Question 1: Simple LSTM Model

Implement a single-layer LSTM of 100 units, that only return last hidden state, followed by a linear Dense layer model using Keras Sequential API to predict the next value. Compare its performance with a simple linear regression model, and a 3 layer MLP of 100 units with relu activation.