import numpy as np

import jax

import jax.numpy as jnp

from jax import grad, jit

from jax.example_libraries import optimizers # for Adam optimizer

from scipy.optimize import minimize

import time

from functools import partial

import pandas as pd

import matplotlib.pyplot as plt

from typing import Tuple

from dataclasses import dataclass

# Set random seed for reproducibility

np.random.seed(42)

jax.config.update("jax_enable_x64", True)

@dataclass

class EarlyStoppingState:

"""State for early stopping and learning rate scheduling."""

best_sharpe: float = float('-inf')

patience_counter: int = 0

best_weights: jnp.ndarray = None

lr: float = 0.1

plateau_counter: int = 0

def generate_data(n_assets: int) -> Tuple[np.ndarray, np.ndarray]:

"""Generate random correlation matrix and expected returns."""

A = np.random.randn(n_assets, n_assets)

corr = A @ A.T

corr = corr / np.max(np.abs(corr))

returns = np.random.randn(n_assets) * 0.1 + 0.05

return corr, returns

# SciPy Implementation remains the same as before

def portfolio_stats_scipy(weights: np.ndarray,

corr: np.ndarray,

returns: np.ndarray,

risk_free_rate: float = 0.02) -> Tuple[float, float, float]:

port_return = np.sum(returns * weights)

port_vol = np.sqrt(weights.T @ corr @ weights)

sharpe = (port_return - risk_free_rate) / port_vol

return port_return, port_vol, sharpe

def negative_sharpe_scipy(weights: np.ndarray,

corr: np.ndarray,

returns: np.ndarray,

risk_free_rate: float = 0.02) -> float:

_, _, sharpe = portfolio_stats_scipy(weights, corr, returns, risk_free_rate)

return -sharpe

def optimize_scipy(corr: np.ndarray, returns: np.ndarray) -> Tuple[np.ndarray, float, float]:

n_assets = len(returns)

constraints = ({'type': 'eq', 'fun': lambda x: np.sum(x) - 1})

bounds = tuple((0, 1) for _ in range(n_assets))

start_time = time.time()

x0 = np.ones(n_assets) / n_assets

result = minimize(negative_sharpe_scipy, x0,

args=(corr, returns),

method='SLSQP',

bounds=bounds,

constraints=constraints)

end_time = time.time()

print('scipy optimization succeed:', result.success)

return result.x, -result.fun, end_time - start_time

# JAX Implementation with Adam

@jit

def portfolio_stats_jax(weights: jnp.ndarray,

corr: jnp.ndarray,

returns: jnp.ndarray,

risk_free_rate: float = 0.02) -> Tuple[float, float, float]:

port_return = jnp.sum(returns * weights)

port_vol = jnp.sqrt(weights.T @ corr @ weights)

sharpe = (port_return - risk_free_rate) / port_vol

return port_return, port_vol, sharpe

@jit

def negative_sharpe_jax(weights: jnp.ndarray,

corr: jnp.ndarray,

returns: jnp.ndarray,

risk_free_rate: float = 0.02) -> float:

_, _, sharpe = portfolio_stats_jax(weights, corr, returns, risk_free_rate)

return -sharpe

@jit

def projection_simplex(x: jnp.ndarray) -> jnp.ndarray:

"""Project onto probability simplex."""

x = jnp.clip(x, 0, None)

return x / jnp.sum(x)

def update_early_stopping_state(state: EarlyStoppingState,

current_sharpe: float,

current_weights: jnp.ndarray,

patience: int = 10,

min_improvement: float = 1e-4,

lr_reduction_factor: float = 0.5,

lr_patience: int = 5,

min_lr: float = 1e-6) -> EarlyStoppingState:

if current_sharpe > state.best_sharpe + min_improvement:

state.best_sharpe = current_sharpe

state.best_weights = current_weights

state.patience_counter = 0

state.plateau_counter = 0

else:

state.patience_counter += 1

state.plateau_counter += 1

if state.plateau_counter >= lr_patience and state.lr > min_lr:

state.lr *= lr_reduction_factor

state.lr = max(state.lr, min_lr)

state.plateau_counter = 0

print(f"Reducing learning rate to {state.lr}")

return state

def optimize_jax(corr: np.ndarray,

returns: np.ndarray,

n_iterations: int = 1000,

initial_lr: float = 0.01, # Lower initial learning rate for Adam

patience: int = 10,

min_improvement: float = 1e-4,

lr_patience: int = 5,

lr_reduction_factor: float = 0.5,

min_lr: float = 1e-6,

b1: float = 0.9, # Adam beta1

b2: float = 0.999, # Adam beta2

eps: float = 1e-8 # Adam epsilon

) -> Tuple[np.ndarray, float, float]:

"""Optimize portfolio using JAX with Adam optimizer."""

# Convert inputs to JAX arrays

corr = jnp.array(corr)

returns = jnp.array(returns)

# Initialize weights and early stopping state

n_assets = len(returns)

init_weights = jnp.ones(n_assets) / n_assets

state = EarlyStoppingState(lr=initial_lr, best_weights=init_weights)

start_time = time.time()

# Initialize Adam optimizer

opt_init, opt_update, get_params = optimizers.adam(

step_size=state.lr,

b1=b1,

b2=b2,

eps=eps

)

opt_state = opt_init(init_weights)

# Gradient function

grad_sharpe = jit(grad(negative_sharpe_jax))

# Optimization loop

for iteration in range(n_iterations):

weights = get_params(opt_state)

weights = projection_simplex(weights) # Project to satisfy constraints

gradient = grad_sharpe(weights, corr, returns)

opt_state = opt_update(iteration, gradient, opt_state)

current_sharpe = -negative_sharpe_jax(weights, corr, returns)

# Update early stopping state

state = update_early_stopping_state(

state,

current_sharpe,

weights,

patience=patience,

min_improvement=min_improvement,

lr_patience=lr_patience,

lr_reduction_factor=lr_reduction_factor,

min_lr=min_lr

)

# Check early stopping condition

if state.patience_counter >= patience:

print(f"Early stopping triggered at iteration {iteration}")

break

end_time = time.time()

final_sharpe = state.best_sharpe

return np.array(state.best_weights), float(final_sharpe), end_time - start_time

def compare_optimizers() -> pd.DataFrame:

"""Compare JAX and SciPy optimizers using logspaced number of assets."""

# Create logspaced array of asset numbers from 5 to 500 with 10 points

asset_numbers = np.unique(np.logspace(np.log10(5), np.log10(500), 10).astype(int))

results = []

for n_assets in asset_numbers:

print(f"Processing {n_assets} assets...")

corr, returns = generate_data(n_assets)

# Run SciPy optimization

scipy_weights, scipy_sharpe, scipy_time = optimize_scipy(corr, returns)

# Run JAX optimization with Adam

jax_weights, jax_sharpe, jax_time = optimize_jax(

corr,

returns,

n_iterations=1000,

initial_lr=0.01,

patience=10,

min_improvement=1e-4,

lr_patience=5,

lr_reduction_factor=0.5,

min_lr=1e-6

)

results.append({

'n_assets': n_assets,

'scipy_time': scipy_time,

'jax_time': jax_time,

'scipy_sharpe': scipy_sharpe,

'jax_sharpe': jax_sharpe

})

return pd.DataFrame(results)

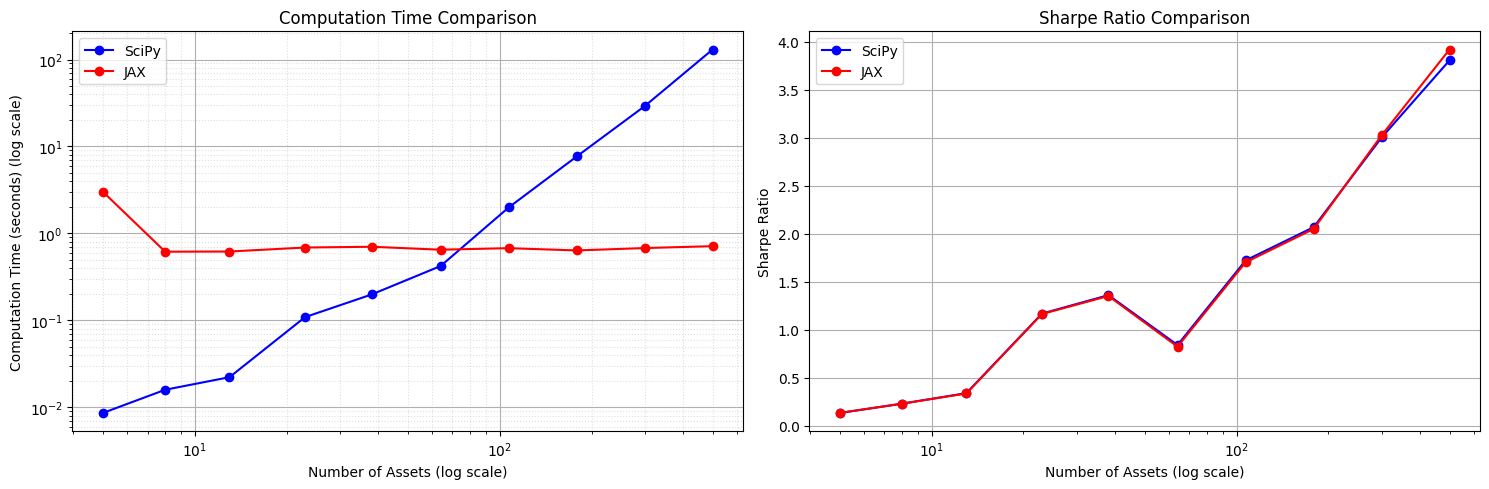

# Run comparison

results_df = compare_optimizers()

# Create visualization

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 5))

# Plot computation time comparison with log scale

ax1.loglog(results_df['n_assets'], results_df['scipy_time'], 'b-o', label='SciPy')

ax1.loglog(results_df['n_assets'], results_df['jax_time'], 'r-o', label='JAX')

ax1.set_xlabel('Number of Assets (log scale)')

ax1.set_ylabel('Computation Time (seconds) (log scale)')

ax1.set_title('Computation Time Comparison')

ax1.legend()

ax1.grid(True, which="both", ls="-")

ax1.grid(True, which="minor", ls=":", alpha=0.4)

# Plot Sharpe ratio comparison with log scale

ax2.semilogx(results_df['n_assets'], results_df['scipy_sharpe'], 'b-o', label='SciPy')

ax2.semilogx(results_df['n_assets'], results_df['jax_sharpe'], 'r-o', label='JAX')

ax2.set_xlabel('Number of Assets (log scale)')

ax2.set_ylabel('Sharpe Ratio')

ax2.set_title('Sharpe Ratio Comparison')

ax2.legend()

ax2.grid(True)

plt.tight_layout()

print("Results DataFrame:")

print(results_df)

print("\nAsset numbers tested:", sorted(results_df['n_assets'].unique()))